Why your tax bill suddenly feels bigger as your business grows

A very common request we get from new clients just joining us, and to be fair a comment we sometimes get from existing clients too.

Michaela gives us some pointers to help discover why tax seems so high and what could be done. But first, in a lot of cases you'll being paying tax because you've taken the money from your business.

As business advisors, we prefer clients to talk to us first when they need to extract more money from the business. We can explore tax-efficiency and need first, but also whether your business can afford the extra strain.

Directors & Shareholders

When we talk about Limited Companies and tax efficiency, we often talk about Director pay. In reality we have to consider the shareholder basis as part of this. We also consider how much work the Director undertakes within the company too, it's not quite as simple as it looks.

Why your tax bill suddenly feels bigger as your business grows

Many business owners reach a point where things are going well. Profits are increasing. Cash in the bank looks healthy. It feels like a reward for all the hard work.

Then the Self Assessment bill lands… and it feels far higher than expected.

If this sounds familiar, you are not alone. There is a very clear reason this happens.

The simple picture

Most directors take a small salary and the rest as dividends. A typical structure might look like:

• Salary: £12,570

• Dividends: the rest of the profits

This is generally the most tax-efficient way to take money from your company.

But as profits grow, something important changes.

What changes as you earn more

The UK tax system is progressive.

• The first slice of your income is tax-free

• The next slice is taxed at basic rates

• The next slice is taxed at higher rates

As your total income increases, more of your dividends fall into the higher rate band, and the tax on those dividends increases accordingly.

A simple illustration

Let’s compare two scenarios.

Scenario 1: Growing business

• Salary: £12,570

• Dividends: £30,000

Most of those dividends sit in the basic rate band. The tax is relatively modest.

Scenario 2: Strong year

• Salary: £12,570

• Dividends: £70,000

Now a much larger portion sits in the higher rate band. The tax jumps more than expected.

Why it feels like a shock

There are a few reasons this catches people out:

• Tax is paid later, often months after the money has been taken

• The increase is not gradual once you cross into higher rate

• Payments on account can mean you are effectively paying towards next year as well

This can turn a good year into a cash flow squeeze if it has not been planned for.

The hidden trap: “just taking a bit here and there”

This is where we see most problems arise.

• A few hundred pounds taken this week

• A larger amount the next

• Something transferred over to cover a personal cost

• Another withdrawal because there is money in the bank

Each amount feels reasonable at the time.

But added together over a year, it can be far more than expected.

Why this causes problems

The key issue is that cash in the bank is not the same as profit.

Your bank balance might look strong because:

• Customers have paid you recently

• VAT or tax has not yet been paid

• Costs are due later

At the same time, your profits may be higher than you realise, which means your tax liability is building in the background.

A better approach to drawings

It does not need to be complicated, but it does need to be intentional.

• Decide what you actually need to take regularly

• Treat that amount consistently, much like a salary

• Avoid dipping in and out without thinking about the impact

• Keep a rough track of what you have taken during the year

A small amount of structure here can prevent a lot of stress later on.

Why it can feel like tax is coming at you from every angle

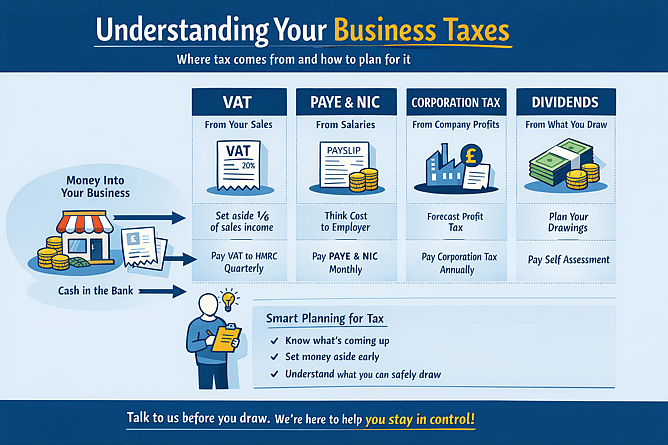

When you are running a limited company, particularly one that is VAT registered and has employees, it can feel relentless.

You may have:

• PAYE to pay monthly or quarterly

• VAT every 3 months

• Corporation Tax once a year

• Self Assessment personally, usually in January and July

They all run on different timelines and do not line up neatly.

Even in a profitable business, this can feel like constant pressure on cash flow.

The real challenge is timing

Most of the difficulty is not the tax itself, but the timing.

Without visibility:

• Cash gets used before tax is set aside

• Liabilities build quietly

• Payments fall closer together than expected

This is where things start to feel tight.

What actually creates each tax

It helps to understand what is driving each bill.

Corporation Tax

Created by company profits. This is based on profit, not cash.

VAT

Created by sales. You are collecting this on behalf of HMRC.

PAYE and National Insurance

Created by paying salaries, including your own.

Dividends (Self Assessment)

Created by what you take personally over and above your salary shown on your payslips.

Payments on account

Created when your personal tax bill increases, requiring advance payments towards the following year.

⸻

Practical ways to stay in control

This is where a few simple disciplines can make a real difference.

PAYE

Think of each pay period as the total cost of employing that person, not just what they receive.

That includes:

• Gross salary

• Employer’s National Insurance

• Pension contributions, if applicable

This is often shown as the “cost to employer” on your payroll reports.

It does not matter that the money is split between the employee, HMRC and the pension provider. It is all leaving your business.

If you put that full amount to one side at the point you run payroll, you will always have what you need when the payment falls due.

VAT

When money comes in from sales, part of it is not yours.

A simple rule for many businesses is to put aside roughly 1/6 of your VAT-inclusive income as it is received.

Once we have prepared your VAT return:

• We take into account VAT on your purchases

• You can release any excess back into the business

For businesses with higher levels of costs, we can help you work out a more appropriate percentage so you still retain the cash flow needed to pay suppliers.

Corporation Tax and Self Assessment

These are the ones that tend to catch people out because they are less visible day to day.

They are driven by:

• Profit in the business

• What you take out personally

The best way to manage these is not to guess.

We can:

• Forecast what you are likely to owe

• Show you when it will be due

• Help you understand what is genuinely available to draw

When to speak to your accountant

The best time to talk is before decisions are made, not after.

It is worth getting in touch when:

• Profits are increasing

• You are taking more out of the business

• You are unsure what you can safely draw

• You are approaching higher rate thresholds

• You are planning a larger withdrawal

My final thoughts

Higher profits are a good thing. A higher tax bill is a sign of that.

But tax works best when it is planned for, not reacted to.

A short conversation at the right time can give you clarity on what you can take, what you need to keep back, and what is coming next. That is what turns tax from a surprise into something manageable.

We also have to consider whether the money going out of a business is earned income or dividends. Limited Companies must declare dividends; these are based on profits (and other factors). You might choose to pay these monthly to help with cash flow, but they have to be recorded correctly as such.

I also see lots of 'advice' suggesting use of various tax loopholes, such as trivial benefits. You should seek proper advice before assuming this is right for you.